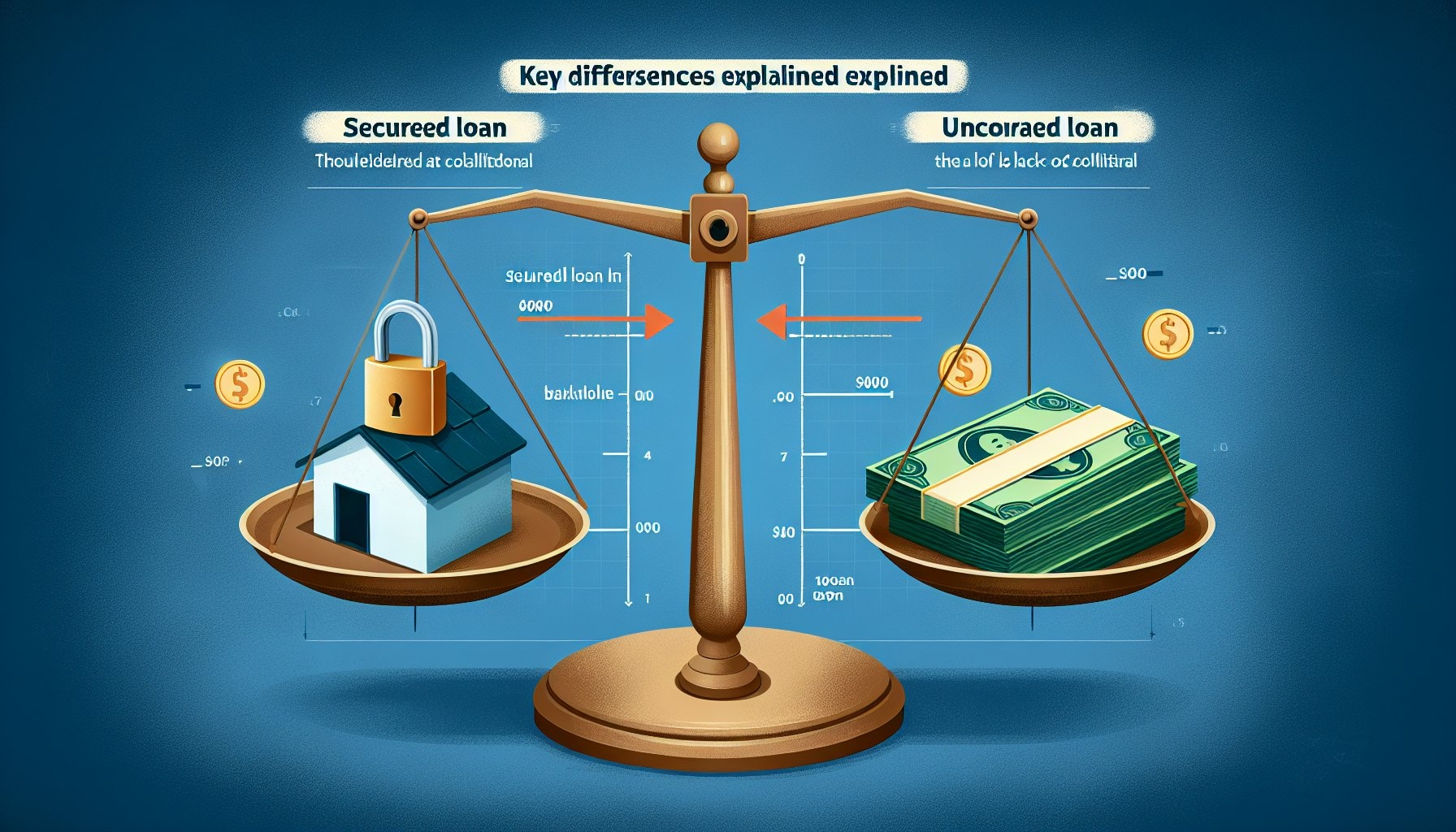

Secured vs. Unsecured Loans: Key Differences Explained

Understanding the nuances between secured and unsecured loans is crucial before making any borrowing decisions. These two loan types represent fundamentally different approaches to lending, impacting everything from interest rates and borrowing limits to repayment terms and potential risks. The primary distinction lies in the presence – or absence – of collateral.

Collateral: The Defining Factor

A secured loan is backed by an asset, known as collateral, pledged by the borrower to the lender. This collateral acts as a guarantee. If the borrower defaults on the loan, the lender has the legal right to seize and sell the collateral to recoup their losses. Common examples of collateral include real estate (mortgages), vehicles (auto loans), and even savings accounts or investment portfolios. The value of the collateral typically matches or exceeds the loan amount, providing the lender with a safety net.

In contrast, an unsecured loan isn’t backed by any specific asset. The lender approves the loan based solely on the borrower’s creditworthiness, income, and financial history. Because there’s no collateral to recover in case of default, unsecured loans pose a higher risk for lenders. Examples include personal loans, student loans, and credit card debt.

Interest Rates: Risk and Reward

The risk associated with each loan type directly influences the interest rates charged. Secured loans typically carry lower interest rates than unsecured loans. This is because the lender’s risk is mitigated by the presence of collateral. If the borrower fails to repay, the lender can seize the asset and sell it to recover the outstanding balance. The reduced risk translates into lower costs for the borrower.

Unsecured loans, on the other hand, come with higher interest rates. Lenders need to compensate for the increased risk of potential losses due to default. The higher interest rates reflect the greater uncertainty involved in recovering the loan amount if the borrower becomes unable to pay.

Borrowing Limits: How Much Can You Access?

Secured loans generally offer higher borrowing limits than unsecured loans. The value of the collateral often determines the maximum loan amount. For instance, a mortgage allows you to borrow a significant sum because it’s secured by real estate, a valuable asset.

Unsecured loans usually have lower borrowing limits. Lenders are more cautious about lending large amounts without collateral to back the loan. The amount you can borrow typically depends on your credit score, income, and debt-to-income ratio.

Repayment Terms: Flexibility and Duration

Secured loans often have longer repayment terms compared to unsecured loans. This is particularly true for mortgages, where repayment periods can extend for decades. The longer repayment terms help to spread out the payments, making them more manageable for the borrower, especially for large loan amounts.

Unsecured loans generally have shorter repayment terms. The shorter durations reflect the higher risk and the relatively smaller loan amounts. Personal loans, for example, often have repayment periods ranging from one to seven years.

Credit Score Impact: Building or Breaking

Both secured and unsecured loans can significantly impact your credit score. Making timely payments on either type of loan can improve your creditworthiness. Conversely, defaulting on payments can severely damage your credit score, making it difficult to obtain future loans or credit.

However, the impact of defaulting on a secured loan can be particularly devastating. Not only will your credit score suffer, but you’ll also lose the asset backing the loan. This can have significant financial consequences, especially if the collateral is your home or vehicle.

Application Process: Documentation and Requirements

The application process for secured loans typically involves more documentation and scrutiny compared to unsecured loans. Lenders need to assess the value and condition of the collateral to ensure it adequately covers the loan amount. Appraisals, inspections, and title searches are common requirements for secured loans.

Unsecured loans often have a simpler application process, focusing primarily on the borrower’s credit history, income verification, and employment status. Lenders will review your credit report, assess your ability to repay the loan, and determine your creditworthiness.

Potential Risks: Default and Foreclosure

The primary risk associated with secured loans is the potential for foreclosure or repossession if you default on the loan. Losing your home, car, or other valuable asset can have severe financial and personal consequences.

The main risk with unsecured loans is the accumulation of debt and the potential for high interest charges. If you struggle to repay the loan, the interest can compound, making it even harder to get out of debt. Additionally, defaulting on an unsecured loan can lead to legal action, such as wage garnishment.

Choosing the Right Option: A Tailored Approach

The best loan type for you depends on your individual financial circumstances, borrowing needs, and risk tolerance. If you have a valuable asset to use as collateral and are comfortable with the risk of losing it, a secured loan may be a good option, offering lower interest rates and higher borrowing limits.

If you don’t have collateral or prefer not to pledge an asset, an unsecured loan may be more suitable. However, be prepared to pay higher interest rates and adhere to stricter repayment terms. Carefully consider your ability to repay the loan before taking on any debt. Thoroughly research different lenders and compare offers to find the best terms and conditions for your specific situation.